- As a martyr

- In a noble sacrifice

- For a crime one didn’t commit

- By plunging into a black hole

- In vain fighting for a great cause

- During a peaceful sleep after a life well lived

Saturday, May 2, 2020

Partial List of The Best Ways to Die

Perhaps apropos in a time of pandemic. Meant not to discourage or disparage. We all will do this eventually.

The Competitive-Efficiency Paradox

A more competition-friendly society will be more efficient (extract more wealth from a given level of resource consumption) which will make it wealthier which will allow it to have more inefficient production. For example, my ability to more cheaply purchase furniture from the finest woodworking craftsmen in the world allows me to myself dabble in woodworking at an uncompetitive, amateur level.

There are two sources of this effect:

I am generally concerned here with the second of these; although, the first is a derivative of the second thus it is in play as well. There are countless examples throughout culture and industry.

Think about this in capital markets. In the past few decades retail-investor trading costs in stocks have plummeted to now be explicitly zero. (Note: if your broker is still charging you a commission for trades, you might need to explore your options.) This massive reduction in cost has allowed a lot more trading to happen--both more traders especially amateurs and more frequent trading. Did this result in increased price-discovery efficiency? Probably some up until a point. But the next new person trading AAPL (Apple Corporation's stock) probably is not bringing new insight into the market. More likely that person is lowering average accuracy ever so slightly. Otherwise, why weren't they trading before this point There is probably enough liquidity in Apple stock so that is not a benefit of an additional trader's trades either.

Here we are suggesting another aspect of this paradox: without easy market entry/exit, we cannot maintain competitive markets. Yet, the next entrant into a highly competitive market is probably likely to be uncompetitive. Ban additional trading or traders for Apple stock and you will unravel quickly the efficiency we have come to enjoy in this highly-competitive market.

Back to the original paradox, is there more efficiency or less? To resolve the problem we should consider it as a continual process as opposed to being linear and finite. We should also expand our understanding of what ends we are achieving. The socialist's fallacy would be to look at two firms both producing cereal and declare this inefficient. "Obviously we could eliminate the duplication as well as the advertising costs by combining the firms," they would proclaim. But this would break the very process that allows for the desired efficiency (higher and higher production at lower and lower cost).

Imagine how disastrous a true socialists should view a marketplace like Etsy. Here the line between hobbyist and profitable craftsman is magnificently blurred. Magnificent because it is the essence of a culturally and materially rich society where experimentation is both allowed and enabled. A society that embraces competition necessarily invites dynamism. This is a foundational principle and an essential characteristic of growth. It is Schumpeter's creative destruction. It is a gift not a curse.

There are two sources of this effect:

- My own wealth growing--call this the personal-income effect.

- Society's wealth growing--call this the production effect.

I am generally concerned here with the second of these; although, the first is a derivative of the second thus it is in play as well. There are countless examples throughout culture and industry.

Think about this in capital markets. In the past few decades retail-investor trading costs in stocks have plummeted to now be explicitly zero. (Note: if your broker is still charging you a commission for trades, you might need to explore your options.) This massive reduction in cost has allowed a lot more trading to happen--both more traders especially amateurs and more frequent trading. Did this result in increased price-discovery efficiency? Probably some up until a point. But the next new person trading AAPL (Apple Corporation's stock) probably is not bringing new insight into the market. More likely that person is lowering average accuracy ever so slightly. Otherwise, why weren't they trading before this point There is probably enough liquidity in Apple stock so that is not a benefit of an additional trader's trades either.

Here we are suggesting another aspect of this paradox: without easy market entry/exit, we cannot maintain competitive markets. Yet, the next entrant into a highly competitive market is probably likely to be uncompetitive. Ban additional trading or traders for Apple stock and you will unravel quickly the efficiency we have come to enjoy in this highly-competitive market.

Back to the original paradox, is there more efficiency or less? To resolve the problem we should consider it as a continual process as opposed to being linear and finite. We should also expand our understanding of what ends we are achieving. The socialist's fallacy would be to look at two firms both producing cereal and declare this inefficient. "Obviously we could eliminate the duplication as well as the advertising costs by combining the firms," they would proclaim. But this would break the very process that allows for the desired efficiency (higher and higher production at lower and lower cost).

Imagine how disastrous a true socialists should view a marketplace like Etsy. Here the line between hobbyist and profitable craftsman is magnificently blurred. Magnificent because it is the essence of a culturally and materially rich society where experimentation is both allowed and enabled. A society that embraces competition necessarily invites dynamism. This is a foundational principle and an essential characteristic of growth. It is Schumpeter's creative destruction. It is a gift not a curse.

Sunday, April 26, 2020

Partial List of Reasons I Can’t Take You Seriously

...(i.e., you can’t have it both ways.)

- You were giving Trump credit (completely dismissive) as the economy was very good 2017-2019, but completely dismissive (strongly blaming Trump) as the economy fell into depression-level problems in 2020. [related]

- You gave Obama credit (didn’t recognize a connection or basically denied it was the case) as the economy recovered following the Great Recession, but refuse to give Trump credit (basically attribute to Trump) as the economy is quite strong for the first three years of Trump’s presidency.

- You were pro (anti) war under Obama but are the opposite under Trump.

- You were fine with (up in arms about) Obama’s trips such as Hawaii and Michelle’s trip to Spain but are the opposite about Trump’s such as Mar-a-Lago.

- You were nonchalant (worried) about Obama’s extensions of executive power but the opposite about Trump’s.

- You were a strong supporter (opponent) of free trade but reversed positions when Trump came into office.

- You want to severely limit and control immigration (guns) based on a few tragic examples but you do not want to do so for guns (immigration).

- You identified and were upset with (lived in denial about) the corruption in the Obama administration but you deny (identify and are upset with) the corruption in the Trump administration.

Sunday, April 19, 2020

Despite or Because

I would like to introduce a new tagline "Despite or Because"--a method of deeper-level thinking.

Specifically, analysis attains sophistication when it is distinguishing between causation and correlation and answering the question: "Is [this result] in spite of or because of [that]?".

The example du jour is COVID-19.

As we stand today a lot remains to be seen including if our efforts will prove successful. Assuming success, we would like to know if the successful flattening of the curve and much below forecast CFR was in fact because of the federal, state, and local governments' lockdown and shelter-in-place orders or despite them?

I'm not just asking if they had no effect. Did they actually impair the battle against the virus? There are three ways I could see the extreme efforts leading to a net harm setting aside the very important social loss of wealth and way of life not to mention that an economy on a strong footing is better able to withstand and respond to a major threat.

Specifically, analysis attains sophistication when it is distinguishing between causation and correlation and answering the question: "Is [this result] in spite of or because of [that]?".

The example du jour is COVID-19.

As we stand today a lot remains to be seen including if our efforts will prove successful. Assuming success, we would like to know if the successful flattening of the curve and much below forecast CFR was in fact because of the federal, state, and local governments' lockdown and shelter-in-place orders or despite them?

I'm not just asking if they had no effect. Did they actually impair the battle against the virus? There are three ways I could see the extreme efforts leading to a net harm setting aside the very important social loss of wealth and way of life not to mention that an economy on a strong footing is better able to withstand and respond to a major threat.

- By putting at risk people into high-dose exposures

- By preventing helpfully-quicker herd immunity

- By disallowing the virus to mutate into a milder strand (this ope is very speculative on my part and I might be very off base here)

Or did those efforts have no meaningful effect period? All of it is interesting and very hard to ask in mixed company much less get open-minded thinking on.

Sweden, South Korea, Taiwan, and perhaps certain states and cities in the U.S. might provide the counter examples as natural experiments we would need to answer this question to some degree of satisfaction eventually.

Sunday, April 12, 2020

The Parallel Problems of TBTF and Poverty

The dilemma faced by central banks specifically and governments generally when considering corporate bailouts and other “market-saving” activities is very similar to the dilemma faced by those designing poverty-relief programs.

Essentially one wants to go with Bagehot’s Dictum: lend liberally on good collateral charging high interest but don’t bail out insolvency. I argue that this has some application to individuals as well as firms. And it applies not just to a central bank or government but really to anyone in a position to help another.

The general view seems to be that those suffering in relative or absolute poverty fall into one of two conditions: (1) Temporarily on hard times (solvent but for liquidity problems) and (2) Permanently unable to provide for oneself (insolvent due to fundamental problems). This was something in my notes from long ago, but it comes into high relief in the current pandemic crisis.

While I have tremendous and from my perspective very atypical faith in individuals' abilities to make the best choices for themselves and to have the corresponding responsibility for such, I do agree that for some people help is needed. For most people who end up in times of need, it is temporary (case 1). For some (few) it is permanent or for very long stretches and to a very large extent (versions of case 2). The dilemma is probably obvious: Is the person(s) in need going to be ultimately and truly helped by my charity or is it simply going to bailout and enable their poor choices? This is not an easy problem to solve. It is typically filled with emotional noise. There are always extenuating circumstances. Hypothetical narratives are easily constructed to fortify confirmation bias. In short it is fraught. And that is when we start with the presumption that there are real-world examples of case 2.

Under what circumstances would we put businesses into case 2? Presumably never except in the case of a truly public good--a rare thing indeed. Yet government's actions and the moral hazard that results implicitly create an environment where case 2 is common and pervasive. We are inappropriately continuing it with airlines, et al.

So this is why I title this as "parallel problems"--because we are making it as such. We are allowing a powerful group with concentrated benefit to dictate the narrative. We should call their bluff. If they are in case 1, then make the argument for being lent to at appropriate interest putting up appropriate collateral. Find a private source of funding even if that private source needs public backing in these extreme times. If they fail, then they were in fact case 2. That doesn't mean they get bailed out. It means they get extinguished to make room for another entity better suited for role they have failed at.

Harsh? Yes indeed. The market is harsh--by design. It is a feature of creative destruction. There is an old saying that in bear markets, stocks return to their rightful owners. The same can more generally be said of capital and economic downturns.

Essentially one wants to go with Bagehot’s Dictum: lend liberally on good collateral charging high interest but don’t bail out insolvency. I argue that this has some application to individuals as well as firms. And it applies not just to a central bank or government but really to anyone in a position to help another.

The general view seems to be that those suffering in relative or absolute poverty fall into one of two conditions: (1) Temporarily on hard times (solvent but for liquidity problems) and (2) Permanently unable to provide for oneself (insolvent due to fundamental problems). This was something in my notes from long ago, but it comes into high relief in the current pandemic crisis.

While I have tremendous and from my perspective very atypical faith in individuals' abilities to make the best choices for themselves and to have the corresponding responsibility for such, I do agree that for some people help is needed. For most people who end up in times of need, it is temporary (case 1). For some (few) it is permanent or for very long stretches and to a very large extent (versions of case 2). The dilemma is probably obvious: Is the person(s) in need going to be ultimately and truly helped by my charity or is it simply going to bailout and enable their poor choices? This is not an easy problem to solve. It is typically filled with emotional noise. There are always extenuating circumstances. Hypothetical narratives are easily constructed to fortify confirmation bias. In short it is fraught. And that is when we start with the presumption that there are real-world examples of case 2.

Under what circumstances would we put businesses into case 2? Presumably never except in the case of a truly public good--a rare thing indeed. Yet government's actions and the moral hazard that results implicitly create an environment where case 2 is common and pervasive. We are inappropriately continuing it with airlines, et al.

So this is why I title this as "parallel problems"--because we are making it as such. We are allowing a powerful group with concentrated benefit to dictate the narrative. We should call their bluff. If they are in case 1, then make the argument for being lent to at appropriate interest putting up appropriate collateral. Find a private source of funding even if that private source needs public backing in these extreme times. If they fail, then they were in fact case 2. That doesn't mean they get bailed out. It means they get extinguished to make room for another entity better suited for role they have failed at.

Harsh? Yes indeed. The market is harsh--by design. It is a feature of creative destruction. There is an old saying that in bear markets, stocks return to their rightful owners. The same can more generally be said of capital and economic downturns.

Saturday, April 11, 2020

Who You Gonna Call? An Economist

If you had questions about the conditions of the local restaurant market, you wouldn't ask a chef or a restaurant manager.

If you had questions about the OPEC oil cartel or how it's actions affect the U.S. fracking industry, you wouldn't ask a petroleum engineer.

If you had questions about the affect charter schools have on education outcomes, you wouldn't ask a teacher.

If you had questions about the pricing and payment of medical services, you wouldn't ask a doctor.

If you had questions about fractional reserve banking, you wouldn't ask a banker.

Well, you might ask these people, and they might have brilliant, insightful answers. But if they did, it would be because they were using the tools and skills of economics. You might be better off just asking an economist--especially one with expertise in the specific area of interest.

Drs. Fauci and Birx are very important experts in immunology. Their understanding of infectious disease and their roles in the current crisis are keys to us conquering SARS-COV-2. But asking them when we should open society back up and revive the economy from the self-induced coma is likely asking them to speak outside their depth. I am not saying they are incapable of performing the necessary trade-off analysis, but if they are, it is because they will be employing economics not epidemiology.

Just as we did not prepare properly for a pandemic, just as we did not heed the warning signs as this one approached, just as we did not do the relevant cost-benefit analysis as decisions were hastily made and virally accelerated, I fear we are not willing to reasonably and scientifically consider, plan, and execute the return to normal life.

Reversing the lockdowns and shelter-in-place commandments should require us to consider the following at a deep level:

What would we like to know includes:

If you had questions about the OPEC oil cartel or how it's actions affect the U.S. fracking industry, you wouldn't ask a petroleum engineer.

If you had questions about the affect charter schools have on education outcomes, you wouldn't ask a teacher.

If you had questions about the pricing and payment of medical services, you wouldn't ask a doctor.

If you had questions about fractional reserve banking, you wouldn't ask a banker.

Well, you might ask these people, and they might have brilliant, insightful answers. But if they did, it would be because they were using the tools and skills of economics. You might be better off just asking an economist--especially one with expertise in the specific area of interest.

Drs. Fauci and Birx are very important experts in immunology. Their understanding of infectious disease and their roles in the current crisis are keys to us conquering SARS-COV-2. But asking them when we should open society back up and revive the economy from the self-induced coma is likely asking them to speak outside their depth. I am not saying they are incapable of performing the necessary trade-off analysis, but if they are, it is because they will be employing economics not epidemiology.

Just as we did not prepare properly for a pandemic, just as we did not heed the warning signs as this one approached, just as we did not do the relevant cost-benefit analysis as decisions were hastily made and virally accelerated, I fear we are not willing to reasonably and scientifically consider, plan, and execute the return to normal life.

Reversing the lockdowns and shelter-in-place commandments should require us to consider the following at a deep level:

Benefit of reduced infection going forward minus Cost of change in way of life

What would we like to know includes:

- R0 - the rate of infection now and going forward (both the average and the distribution of typical people and super-spreaders); Robin Hanson's analysis shows the need for an even deeper level of thought.

- How did R0 changed over time both as a result of human action and public policy as well as naturally?

- How many people were infected and when?

- How did the various policies impact viral transmission, viral impact (did putting asymptomatic infected people, mostly kids, in intense contact with at-risk people, mostly elderly, cause dangerously strong infections--dose makes the poison?), other health results, etc.?

- How did the various policies impact our way of life? Just how damaging were the policies and how damaging was the virus?

- What would we do different? How many lives on net did the actions taken save? How much was overall well being benefited by the actions taken?

- How would we do it differently in the future?

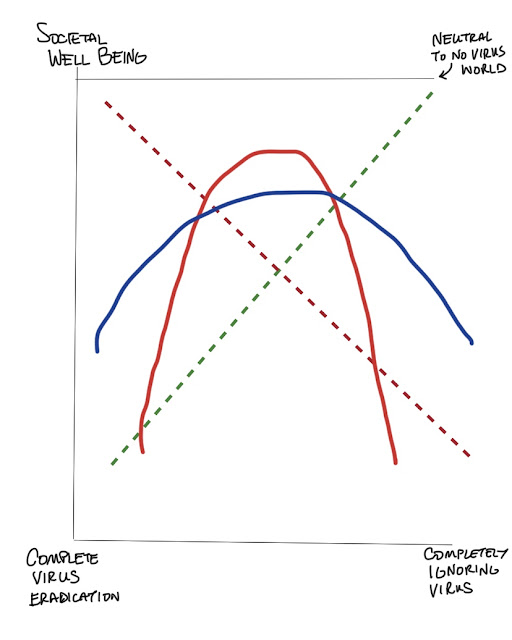

At this point we don't really know enough to depict the overall tradeoffs and how the equation above would plot in the graph below.

The x-axis runs from maximum virus eradication (all resources thrown at fighting the virus, which is well beyond even the extreme measures we have taken so far) to not changing our lives one bit other than perhaps dealing with infections as they arise including hospitalizations and death. The y-axis is overall societal well being. In the middle is the point of well being that is equal to a world where there was no SARS-COV-2.

Is the trade-off function like one of the solid-line parabolas? Don't get too hung up on the lines I've drawn other than to notice that one is at times above the other. And of course choices we make could allow us to jump from one trade-off frontier to another. But notice the other two stylized functions. Perhaps the virus is so dominant that any effort short of total effort to counter it was a net loser for societal well being (as depicted in the red-dashed line). This is possible but highly unlikely. Yet this in the extreme is the position implied by many in the populace as well as some in power. Alternatively, the virus could be an unfortunate circumstance but not one that at any level deserves us changing our way of life (as depicted in the green-dashed line). This is also possible but highly unlikely. Yet this in the extreme is the position implied by those who might be labeled virus deniers.

We would expect, however, that some type of parabolic function if not one with multiple peaks would properly depict the real world tradeoffs. The devil is in the details, and which function and how we might transform the function to improve our lot is the many-trillion-dollar question. I would like to see it asked more strongly and widely, and I would especially like to see it asked of economists.

The x-axis runs from maximum virus eradication (all resources thrown at fighting the virus, which is well beyond even the extreme measures we have taken so far) to not changing our lives one bit other than perhaps dealing with infections as they arise including hospitalizations and death. The y-axis is overall societal well being. In the middle is the point of well being that is equal to a world where there was no SARS-COV-2.

Is the trade-off function like one of the solid-line parabolas? Don't get too hung up on the lines I've drawn other than to notice that one is at times above the other. And of course choices we make could allow us to jump from one trade-off frontier to another. But notice the other two stylized functions. Perhaps the virus is so dominant that any effort short of total effort to counter it was a net loser for societal well being (as depicted in the red-dashed line). This is possible but highly unlikely. Yet this in the extreme is the position implied by many in the populace as well as some in power. Alternatively, the virus could be an unfortunate circumstance but not one that at any level deserves us changing our way of life (as depicted in the green-dashed line). This is also possible but highly unlikely. Yet this in the extreme is the position implied by those who might be labeled virus deniers.

We would expect, however, that some type of parabolic function if not one with multiple peaks would properly depict the real world tradeoffs. The devil is in the details, and which function and how we might transform the function to improve our lot is the many-trillion-dollar question. I would like to see it asked more strongly and widely, and I would especially like to see it asked of economists.

Saturday, April 4, 2020

Some Secrets to Investing Success

To be a "successful" investor, you've got to start by defining success. It is different for just about everyone. Two investors with nearly identical demographics including age, lifestyle, and net worth can have significantly different financial goals. And financial goals are almost never determined along one dimension. Thinking they are is a formula for a typical 80s movie, and most were bad depictions of how investing works even though they have classic status.

Here are five hot tips to get you a leg up on the competition:

1. Get a head start. As a Sooner I can tell you there is no substitute.

Here are five hot tips to get you a leg up on the competition:

1. Get a head start. As a Sooner I can tell you there is no substitute.

Imagine you, a very conservative person, begin investing at age 25 by putting $100 per month into a very safe bond index fund (perhaps BND). You do this for 20 years (240 months straight). Let's suppose this bond investment grows at an average rate of 3.5% per year. Although you put in $24,000 of your own money, that money is growing on average as it is invested. So after the 240th month you would expect to have about $34,576 of which about $10,576 is the growth of the investment. At that point when you are 45 years old you stop saving additional money and just let the bond investment grow for the next 20 years or until you are 65 years old (40 total years of investing).

Now imagine me, a rather aggressive person the same age as you, waits until you are done putting money in to begin my own investing. At that point, 20 years after you started, I start investing $100 per month and I don't stop adding $100 per month until age 65 (20 years of adding to my investment just like you) and I invest in a stock fund with more risk and return potential (perhaps VT). Let's suppose this stock investment grows at an average rate of 8% per year--more than double your investment return per year. After 240 months I've added just as much as you, $24,000 of my own money. I've also enjoyed a higher rate of return on those investments. But do I have as much in total? In this case, no.

At age 65 you have over $68,798 while I have only $57,266. And if you would have chosen the stock fund instead of the bond fund keeping the other assumptions the same, you would have over $266,914--being early is an amazing difference!

See the chart below and notice how starting early allowed you to be invested more conservatively.

Here is a short video showing the same principles at work.2. Protect against the downside first and foremost.

It is mathematically impossible to save enough and earn enough on that savings to cover spending more than you have. Try it and see. If you save $20 million and earn a return of $40 million on it (a 200% rate of return!), you still cannot spend $61 million. Even if you borrow against the $60 million to try and get an additional $1 million, you have to come up with that $1 million to pay back the loan. Spending prudence should seem self evident. So too should investing prudence because you mathematically cannot spend investment earnings you do not achieve.

If I put all my investment (eggs) into one stock or bond (basket so to speak) and that stock or bond goes broke, my investment is gone. If I put all my investment into two stocks or bonds and one of those goes broke while the other is fine, I have only lost half of my investment. Repeat this logic for more and more individual investments, and you will eventually get to a point of diversification where the impact of picking a complete lemon (stock or bond that goes to zero) is immaterial to you. That should be a goal for most investors.

The entire stock or bond market basically cannot go to zero. If it does, you got bigger problems than your IRA balance like the colossal asteroid that must have struck the Earth. In fact, the history of economic growth has been a reliable (eventual) pattern of higher highs and higher lows. Diversification is your first best risk reducer against the threat of ruin.3. Grab the right rate of return.

It is all about beta not alpha. Beta is the fancy way of saying give me the market's performance. Alpha is the fancy way of saying give me something different (hopefully better) than the market's performance. Beta is passive investing, boring, dull, easy, anybody can do it. Alpha is the sexy stuff. Alpha is the smart money, the guys zigging when the panicked sheep are zagging. At least, that is the story so many like to tell.

The fact is overwhelmingly most professional money managers do not beat their benchmark. Let that sink in--the guys paid millions of dollars to add value for investors by being better than their benchmark are most of the time subtracting value. Investors are paying a fee to get a lower rate of return than they could otherwise.

The key decision for most investors is not "can I beat the market?" but rather "can I be the market, and what market do I want to be?" Remember, every investor is different--different risk tolerances, different various goals, different unique circumstances and biases, etc. Getting the right mixture of various investments (AKA, asset allocation) is the first best method of achieving your financial goals--notice how this works hand in glove with diversification. The asset allocation decision will almost exclusively determine the risk/return path your investments travel making other decisions small contributors to performance.4. Look for the rewards of liquidity and transparency.

Listen to Jason Zweig among so many others. Don’t trust hedge funds. Understand that private equity = public equity minus liquidity minus transparency plus fees plus leverage. As Cliff Asness points out, let others accept a discount for illiquidity (when a premium would be the theoretical demand of investors). You want access to your money while invested in assets and processes you can understand, fully benchmark against, and truly see the value of.5. Resist temptation and envy--the key drivers of FOMO.

This one has many short sub components (here are a few):

The bottom line of this is successful investing generally is simpler, cheaper, and duller than advertised.

- Don't time the market -- This is an impossible task and anyone who tells you different is a liar or a fool.

- Therefore, stay invested and on your long-term plan -- Uncle Freddy very likely doesn't know something you should be emulating. This time (any time) is very probably NOT a time to go to (some different asset allocation as compared to your long-term plan).

- You will never be significantly invested in the best performing single investment because of rules 2 & 3 above -- You don't want the risk that has only luck as its investment thesis.

Subscribe to:

Posts (Atom)